Most insurance executives don't wake up wanting a new software platform. They wake up to bottlenecks. A claims team rekeys the same data into three systems. Underwriters wait on documents trapped in email chains. Compliance asks for an audit trail, and staff pull screenshots instead of reports. Meanwhile, leadership hears the same refrain from every department: we can't move faster because the systems don't talk.

That's the context for custom insurance software solutions. This isn't about buying shinier screens. It's about replacing operational friction with a system designed around how your business works.

There's also a second pressure building at the same time. Teams want AI for document handling, claims triage, and service automation, but regulated environments can't treat AI like a browser plugin. Once models touch customer data or influence decisions, you need governance. You need prompt control, access rules, logging, and cost visibility. Without that layer, AI creates as many risks as it removes.

Beyond Patchwork Systems The New Reality of Insurance Tech

A lot of insurers still operate like a house that's been renovated one room at a time over twenty years. The kitchen works. The lights mostly work. But behind the walls, the wiring is a mess.

That patchwork usually looks familiar. One system for policy administration. Another for claims. A billing tool that was customized beyond recognition. A portal that only partially reflects back-office data. Then a spreadsheet layer appears to hold everything together.

Why the old model breaks down

These environments don't just slow people down. They create conflicting versions of the truth. A claims adjuster sees one status. Customer service sees another. Compliance sees missing fields. Executives see delayed reporting.

Custom insurance software solutions address that by treating the platform as one operating environment instead of a collection of disconnected tools. Policy administration, underwriting, claims, compliance, billing, and self-service can work as coordinated parts of the same system.

Here's why that shift is accelerating. 84% of new insurance system purchases are cloud-based, and the global insurance software market is projected to grow from USD 15.03 billion in 2026 to USD 20.41 billion by 2031, according to industry figures summarized by CrossAsyst.

Custom software matters most when the business model is complex enough that “good enough” workflow creates recurring operational drag.

AI raises the stakes

Modernization now includes more than cloud migration. Many insurers want AI to handle intake, document extraction, and internal search. That makes sense. But AI inside insurance operations needs administrative discipline.

A useful mental model is this: the model is the engine, but governance is the dashboard, brakes, and black box recorder.

Without those controls, teams run into familiar problems:

- Prompt drift: Different teams use different instructions and get inconsistent outputs.

- Security gaps: Sensitive data reaches tools without clear access boundaries.

- No auditability: Leaders can't explain what the AI saw or why it responded the way it did.

- Cost surprises: Usage expands faster than anyone expected.

That's why insurers modernizing for AI usually need a management layer, not just a model connection.

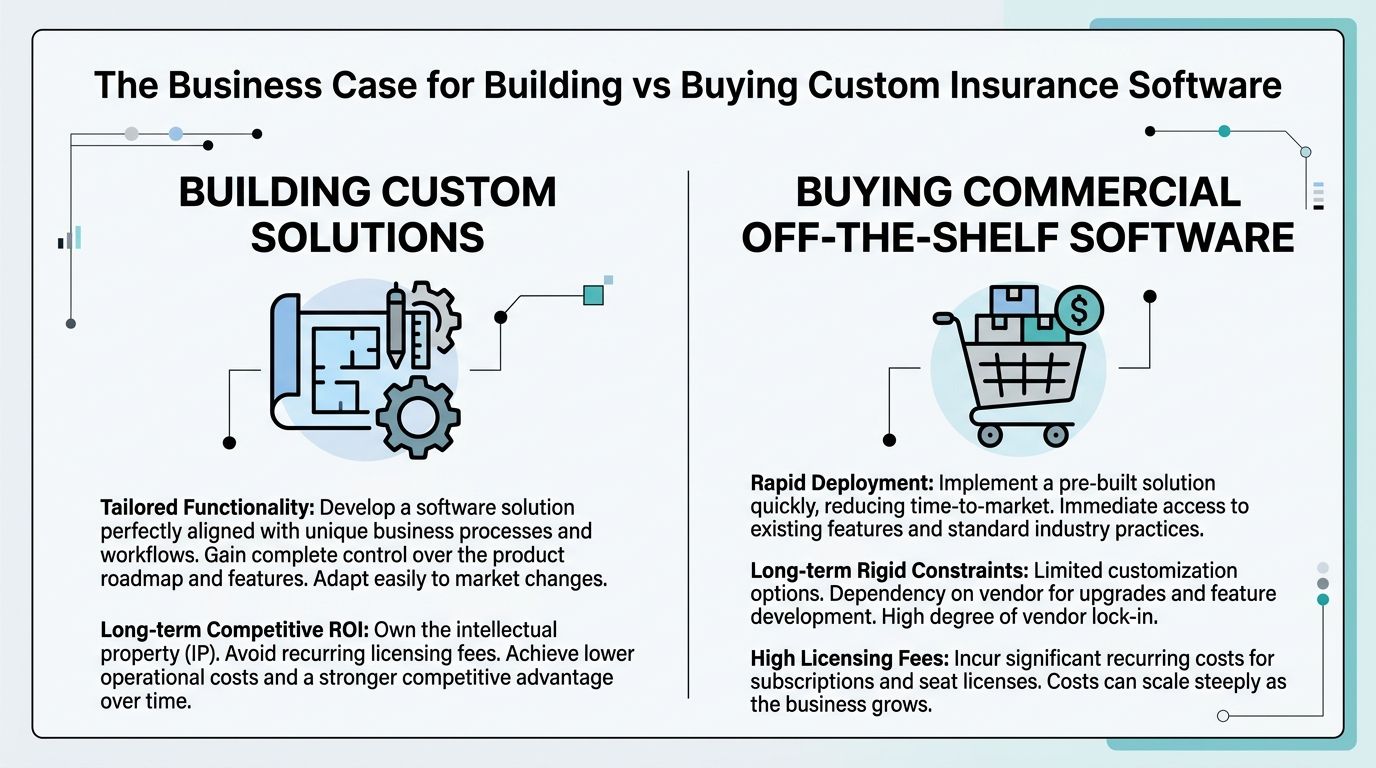

The Business Case for Building vs Buying

The first executive question is usually blunt and correct: why not just buy another packaged platform?

Sometimes buying is the right move. If a process is standard and not strategically important, off-the-shelf software can work. But insurance rarely stays standard for long. Product rules differ by line. Regional compliance varies. Internal approval logic grows around edge cases. Acquisitions add another layer. A generic workflow that looks fine in a demo often becomes expensive workarounds in production.

Where custom wins

Custom software tends to make sense when your workflows are part of how you compete or how you stay compliant. It lets you shape the process around the business rather than asking the business to adapt to vendor defaults.

A concise way to frame the decision:

| Approach | Best fit | Common tradeoff |

|---|---|---|

| Buy | Standardized needs, fast deployment | Lower flexibility over time |

| Build custom | Complex workflows, integration-heavy environments | More upfront planning |

| Hybrid | Keep core systems, build strategic layers around them | Requires good architecture discipline |

The financial case is stronger than many leaders expect. A summary of Nucleus Research findings cited by Neontri reports an average ROI of 122.22%, with break-even typically between 8 and 14 months for custom insurance software. The same source notes that AI-powered underwriting tools can improve risk assessment accuracy by up to 20%, and automated claims platforms can cut processing times by 40%. You can review those figures in this custom insurance software analysis from Neontri.

Buying looks cheaper until process friction compounds

License cost is only one part of the equation. Leaders also have to count manual reconciliation, duplicate entry, training on awkward workflows, audit preparation, and the backlog of “small exceptions” that never stay small.

Practical rule: If your team keeps building side processes outside the platform, the platform isn't really cheaper.

A custom approach can also support broader platform strategy. If you're weighing the long-term tradeoffs, Wonderment's guide to custom software development benefits is a useful companion read.

In non-technical terms, buying software is like leasing a prebuilt warehouse. Building custom is like designing the loading docks, racking system, and floor plan around how your operation moves inventory. If movement is your business, layout matters.

Core Features and Modern Software Architectures

A modern insurance platform doesn't need to be one giant application. In fact, that's often the wrong approach. The better model is a set of connected services, each doing a specific job well.

These solutions function as modular building blocks, governed by specific rules. One block manages policy data. Another handles claims intake. Another runs underwriting logic. Another serves customer portal functions. They connect through APIs, which are structured ways for systems to exchange data and actions.

The core building blocks

Most custom insurance software solutions include a variation of these capabilities:

- Policy administration: Product setup, endorsements, renewals, cancellations, and status management.

- Claims management: FNOL intake, assignment, documentation, workflow routing, and resolution support.

- Underwriting tools: Risk rules, referral triggers, data enrichment, and approval workflows.

- Billing and payments: Invoicing, collections, payment status, and financial reconciliation.

- Document management: Storage, retrieval, extraction, and version tracking.

- Customer and agent self-service: Portals and mobile access for status checks, uploads, and requests.

The key isn't that these functions exist. Most platforms have them. The key is that the business rules behind them are specific to your operation.

Why architecture matters to executives

Architecture sounds technical, but the business effect is easy to understand. Good architecture lets you change one area without breaking five others.

That matters when you want to launch a new portal, add mobile features, or experiment with AI-enabled workflows. According to LaSoft's overview of bespoke insurance platforms, these systems can integrate with legacy core systems and third-party data sources without forcing a full rip-and-replace approach. That reduces disruption and lets teams layer new mobile, portal, and AI capabilities on top of existing backbones.

Here's the executive translation:

- APIs reduce rework: Systems exchange data directly instead of relying on exports and emails.

- Service-based design limits blast radius: Updating claims logic doesn't require rewriting the customer portal.

- Phased modernization lowers risk: You can replace the worst bottleneck first, not rebuild the company in one motion.

If you want a plain-English primer on designing those foundations, this article on software architecture best practices is helpful.

A good insurance platform should behave less like a monolith and more like a well-run operations center. Each team has its station, but everyone works from the same playbook.

Where agentic AI fits

There's growing interest in systems that don't just answer questions, but coordinate actions across workflows. That's where teams start to develop agentic AI systems that can route tasks, gather context, and assist humans across multiple steps.

In insurance, that only works when the surrounding architecture is clean. If your data is fragmented and your rules live in tribal knowledge, an AI layer won't fix the mess. It will inherit it.

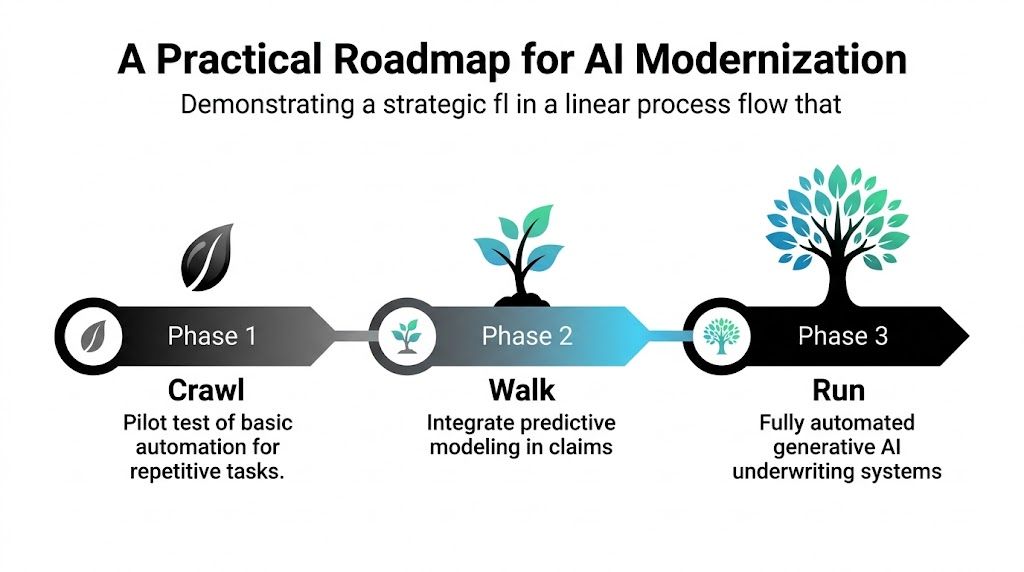

A Practical Roadmap for AI Modernization

Most AI discussions in insurance jump too quickly to flashy use cases. The better question is simpler: where will automation remove real work first?

The most reliable starting point is high-volume, document-heavy work. That's also the gap many articles miss. A benchmarked roadmap matters because insurers need a practical sequence, not a pile of features. As noted in this analysis of insurance AI priorities from TOXSL, teams should start with high-volume, document-heavy tasks to reduce cycle times, then expand into decision support with human-in-the-loop controls and cost management.

Crawl with repetitive document work

The first phase should target work that is repetitive, rules-based, and easy to review.

Good examples include:

- FNOL intake support: Extract key fields from submitted forms and route them for review.

- Document classification: Sort incoming claims files, correspondence, and evidence into the right workflow.

- Data extraction: Pull policy numbers, dates, names, and loss details from structured and semi-structured documents.

If you're evaluating tooling for handling high-volume insurance documents efficiently, focus on systems that support validation checkpoints instead of fully automated black-box decisions.

Walk into guided decision support

Once the organization trusts the data flow, AI can assist with prioritization and recommendations.

That usually means:

| AI stage | Best use | Human role |

|---|---|---|

| Crawl | Extract, classify, summarize | Verify output |

| Walk | Triage, prioritize, recommend | Approve or override |

| Run | Coordinate complex workflows | Govern policy and exceptions |

At this stage, AI can help surface missing documents, suggest claim routing, or support underwriting review with structured summaries. It shouldn't replace accountable staff. It should shrink the amount of low-value review work.

Run with governance, not just automation

The third phase is where many programs stall. The issue usually isn't model quality alone. It's control.

To scale AI in insurance, leaders need a clear view of:

- Prompt versions: Which instruction set produced which output.

- Parameter access: What internal data the model could use.

- Logging: What happened, when, and in which workflow.

- Spend visibility: How usage changes by team, process, or model.

That's one reason teams exploring AI modernization often pair implementation planning with a broader application modernization roadmap. AI only works well when the surrounding system is designed for traceability.

Navigating Complex Compliance and Security

Insurance leaders don't need to be persuaded that compliance matters. They need to know why custom architecture can reduce risk more effectively than bolted-on controls.

The answer is straightforward. In a generic system, compliance often lives in checklists, manual reviews, and after-the-fact reporting. In a custom system, controls can be built directly into the workflow itself.

Build controls into the path of work

That means role-based access can determine who sees what. Encryption can protect data in the right places. Audit logging can capture actions automatically. Policy validation can happen during submission instead of during remediation.

According to Decerto's review of custom insurance platforms, organizations using custom insurance solutions see 40% to 60% fewer compliance violations and 55% lower data breach costs because compliance checks, access control, and audit logging are designed into the system from the ground up.

Compliance is cheaper when the system prevents bad actions than when the business has to investigate them later.

What this looks like in practice

For a non-technical executive, it helps to picture three layers:

- Access layer: Users only see the records and actions tied to their role.

- Rules layer: Required steps, validations, and approvals happen automatically.

- Evidence layer: The system records what changed, who changed it, and when.

That architecture is especially useful in environments dealing with changing privacy and healthcare-related requirements, including regulations such as GDPR and HIPAA.

If your leadership team is also reviewing external risk posture, this guide on cyber protection for Canadian firms offers a practical perspective on how cyber exposure and insurance readiness intersect.

Security should support speed

Executives sometimes assume stronger controls will slow the business down. Poorly designed controls do. Embedded controls usually do the opposite because they remove manual checkpoints and reduce exception handling.

A claims handler doesn't need to remember every rule if the system enforces the important ones automatically. That's better for compliance, and it's usually better for cycle time.

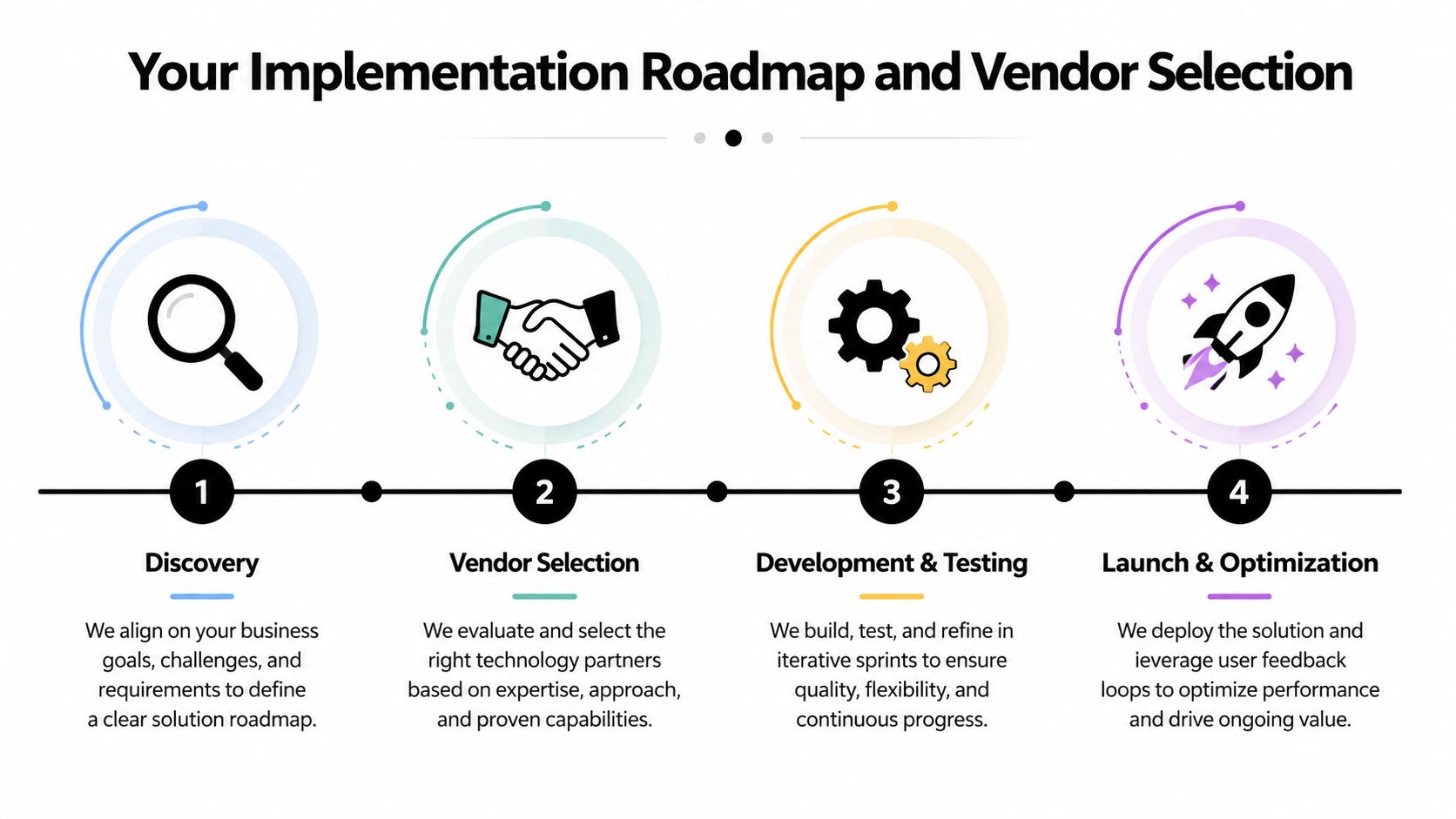

Your Implementation Roadmap and Vendor Selection

Large software projects become risky when leaders treat them like a single event. They work better as a sequence of decisions.

The implementation path for custom insurance software solutions usually follows four phases. Each phase should answer one business question before the next starts.

Phase one and two

Discovery and strategy come first. During this phase, teams define the operational problem in business terms. Not “we need a platform,” but “we need to reduce handoffs in claims intake,” or “we need underwriting decisions to follow a consistent rule path.”

Vendor selection comes next, and many buyers then focus too much on price. Insurance software work is rarely just software delivery. It's process design, integration planning, security thinking, and change management.

A strong partner should be able to discuss all of the following in plain language:

- Insurance workflow knowledge: They understand policy, claims, service, and compliance patterns.

- Architecture choices: They can explain why a service should be separate, integrated, or deferred.

- AI governance readiness: They know how prompts, logs, and data access should be managed.

- Delivery discipline: They work in iterations and show progress early.

Phase three and four

Development and testing should happen in increments. A portal, intake flow, or internal operations tool can be released in stages instead of waiting for one giant launch. That reduces adoption risk and exposes bad assumptions earlier.

Launch and optimization is essential for safeguarding value. Teams need post-launch support, user training, and a feedback loop. A system that is technically live but poorly adopted is still failing.

Selection shortcut: Ask every vendor how they would modernize one workflow without disrupting the systems you must keep. The quality of that answer tells you more than a polished demo.

A practical vendor checklist

Use this scorecard when evaluating candidates:

| Question | Why it matters |

|---|---|

| Can they integrate with legacy systems instead of demanding replacement? | Reduces operational risk |

| Can they explain their AI control model? | Protects compliance and costs |

| Do they show user flows, not just architecture diagrams? | Improves adoption |

| Do they offer support after launch? | Keeps the platform useful |

| Can they talk to executives and operators with equal clarity? | Prevents project drift |

Good vendors don't just promise delivery. They help leadership make fewer bad decisions along the way.

Unlock True AI Potential with Smart Management

AI in insurance gets harder as soon as it becomes useful. One team wants document summaries. Another wants claim routing support. A third wants underwriting assistance. Suddenly, the organization isn't managing one model experiment. It's managing a portfolio of AI behaviors tied to real operations.

That's where an administrative layer becomes necessary.

One option in this category is Wonderment Apps, which offers a prompt management system designed to plug into existing software as part of AI modernization. The system includes a prompt vault with versioning, a parameter manager for internal database access, logging across integrated AIs, and cost management for cumulative usage tracking.

What that solves

Those functions matter because they answer practical executive concerns:

- Consistency: A versioned prompt vault helps teams avoid one-off instructions scattered across departments.

- Security: A parameter manager creates a cleaner path between AI workflows and internal data access.

- Traceability: Logging helps teams review what happened across integrated AI actions.

- Spend control: Cost dashboards make it easier to see where usage is growing.

This isn't about making AI more exciting. It's about making it governable.

For insurance organizations, that distinction matters. AI can support service, underwriting, and claims operations, but only if leaders can control how it behaves, how it connects, and what it costs. The companies that get value from AI usually aren't the ones with the most pilots. They're the ones with the clearest operating model.

If you're planning custom insurance software solutions and want a practical way to modernize with AI controls in place, Wonderment Apps can walk you through the architecture, governance, and management layer in a live demo.